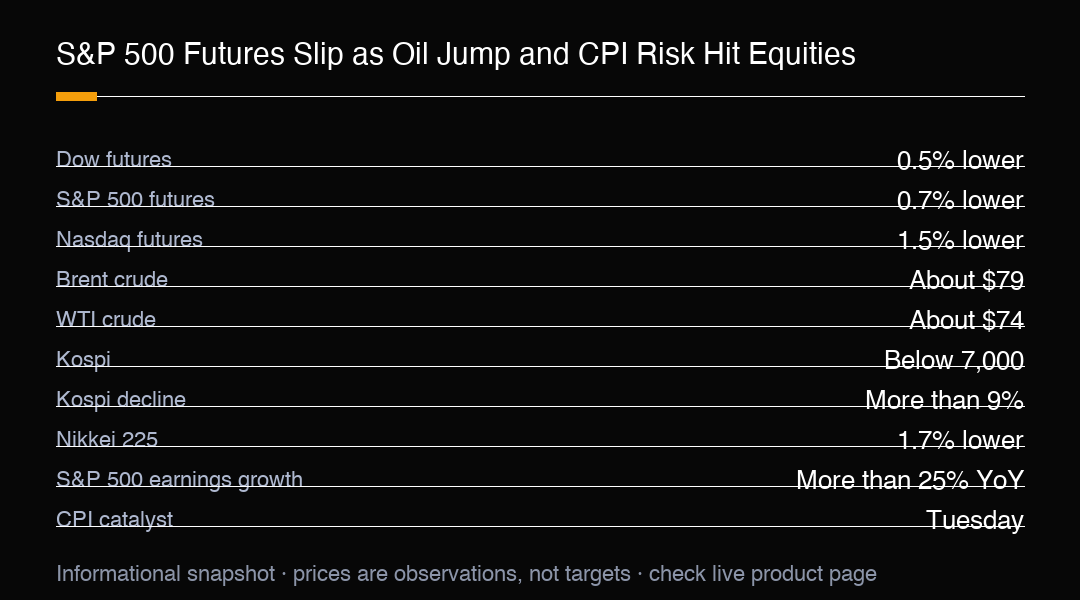

S&P 500 futures fell 0.7% early Monday as renewed geopolitical tension weakened risk appetite and sent a fresh shock through Asian markets. Dow futures slipped 0.5%, while Nasdaq futures dropped 1.5%, showing the pressure was broad but heaviest in growth-sensitive contracts. These are futures indications, not cash-index closes, and the setup for US500 traders is a cross-asset risk-off move in which geopolitics, oil, and inflation data are being priced together.

The geopolitical claims remain fluid, so traders should avoid treating any single statement as a permanent market fact. The key mechanism is that uncertainty around conflict and shipping can lift the risk premium in energy. Brent crude jumped about 4% toward $79 a barrel, while West Texas Intermediate gained more than 3% to around $74. A larger oil move can revive inflation concerns just as a major US data catalyst approaches.

Higher fuel costs can raise transportation and production expenses, and a persistent oil increase can make inflation progress look less secure. That may keep central banks cautious and limit confidence in rapid policy easing. For the S&P 500, the result is a valuation question as much as an earnings question: if yields rise because inflation risk returns, high-duration growth shares can face pressure even when company-level demand stays solid.

Asian markets showed how fast the mechanism spreads. South Korea's Kospi plunged more than 9% and fell below 7,000, its lowest level since early May. The Kosdaq lost 2%, and Japan's Nikkei 225 slid 1.7%. Those moves reflect both regional risk and the sensitivity of technology-heavy markets to global growth expectations, and they give US index traders a useful pre-market signal.

The depth of the Kospi move is worth a closer look because it was not a gentle decline. A drop of more than 9% in a single session is the kind of displacement that can trigger its own momentum, as leveraged accounts are forced to deleverage and volatility sellers are caught offside. When a major regional index falls below a round level like 7,000, it also becomes a psychological reference that can attract both bargain hunters and continued sellers, so the direction from here depends on whether the initial shock is absorbed or extended.

The US earnings calendar adds two-way risk. JPMorgan, Goldman Sachs, Morgan Stanley, Bank of America, Citigroup, Wells Fargo, Netflix, Johnson & Johnson, and UnitedHealth are scheduled to report this week. Analysts project second-quarter S&P 500 earnings growth of more than 25% year over year, but that is an expectation, not a result. Strong earnings could help sentiment absorb higher oil; disappointing guidance could magnify the macro pressure.

The combination of a high earnings bar and a fresh macro shock is exactly the setup that tests conviction. More than 25% projected growth sets a demanding comparison, and any company that merely meets estimates can be punished if the macro backdrop is already fragile. At the same time, a soft inflation print or calming geopolitical headline could let strong results do the heavy lifting. Traders should watch whether the index reacts to the earnings themselves or to the macro narrative wrapped around them.

Tuesday's June CPI report is the next major test. A hotter reading could reinforce the higher-for-longer rate narrative, especially if oil stays elevated. A softer reading could support a relief move in futures, but the reaction may still depend on geopolitical headlines and earnings positioning. CPI is a catalyst, not a guaranteed direction signal.

For US500 positioning, the gap between futures and cash matters. A 0.7% futures decline shows how risk is priced before the main session, but it does not guarantee the cash index opens or closes at the same level. Overnight liquidity can exaggerate moves, and new information can reverse them. Scenario planning should include a continuation lower, a gap-and-recover pattern, and a relief rally that stalls near resistance.

Oil is the key cross-asset reference. Brent near $79 and WTI near $74 show investors assigning a meaningful premium to supply and conflict risk, but those levels can move quickly if the shipping situation changes. A sustained oil rise keeps inflation and yields in focus; a fast retreat could remove some pressure from equity futures without repairing weak breadth.

Risk control should account for event clustering. Geopolitical headlines can arrive outside trading hours, CPI can reprice rates and indices fast, and earnings can produce sharp single-stock moves that affect index breadth. Traders should avoid reading one overnight price as the full US session, and should wait for follow-through across sectors.

The practical takeaway for index traders is to treat Monday's futures move as a warning rather than a verdict. A 0.7% overnight decline is informative, but the cash session can diverge once US earnings and the inflation picture are in view. The most useful signals will be whether the S&P 500 can hold a bid into the CPI print, whether megacap technology stabilises after its heavier Nasdaq-led drop, and whether oil stays bid enough to keep the rate-risk narrative alive.

Breadth is especially important because index futures can hide internal weakness. A small group of large companies can support headline levels while banks, industrials, and smaller technology names keep falling. Traders should treat the futures percentage as an opening risk gauge and use cross-sector participation to judge whether the move becomes a broader trend.

The current S&P 500 futures setup is a test of cross-asset resilience. A 0.7% decline sits between the smaller Dow move and the heavier Nasdaq move, while oil near $79 Brent and $74 WTI raises the inflation stakes. More than 25% projected earnings growth may support sentiment, but Tuesday's CPI and this week's results still need to validate it. MC Markets traders can use US500 to monitor those scenarios. This is market commentary, not personal financial advice.

Trading Insight

S&P 500 futures are pricing a cross-asset risk-off test: 0.7% lower for the S&P 500, 1.5% lower for Nasdaq, Brent near $79, WTI near $74. The Kospi fell more than 9% below 7,000, and analysts see more than 25% earnings growth. Tuesday's CPI can shift rate expectations quickly. Watch whether a futures rebound broadens beyond mega-cap names. This is market commentary, not personal financial advice.