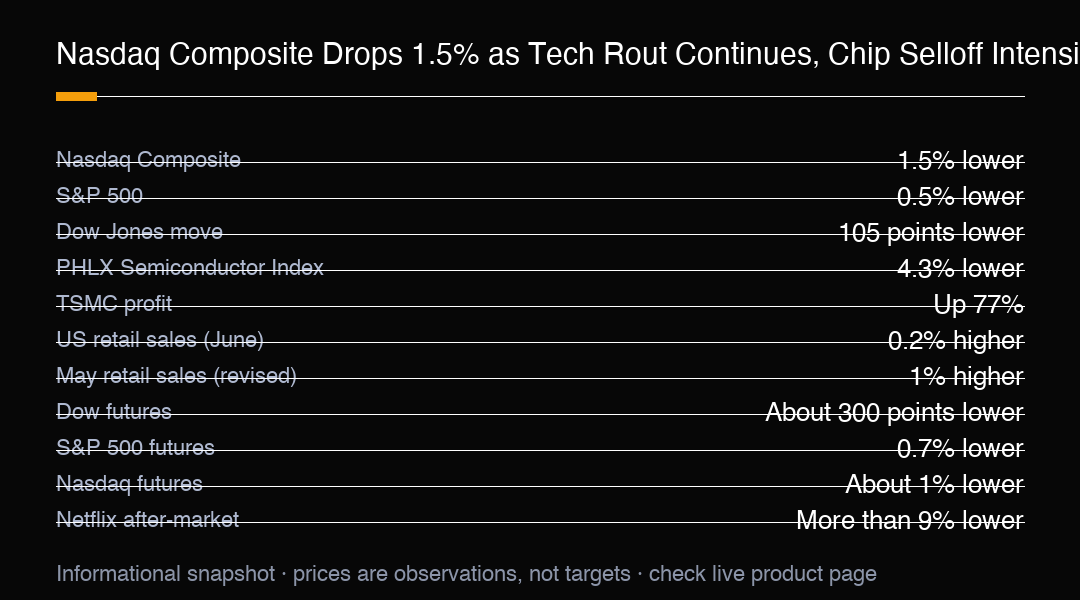

US stocks are headed for a losing week just as the earnings season is about to get interesting. The Nasdaq Composite slid 1.5% on Thursday, leading Wall Street lower as the chip selloff gathered fresh momentum, and the weakness left the broader market on the back foot heading into a busy reporting stretch.

The S&P 500 lost 0.5%, while the Dow Jones Industrial Average slipped 105 points, or 0.2%. Not every stock had a bad day, but technology clearly bore the brunt of the selling. Investors have spent months piling into the same handful of tech winners, and now they are doing the opposite. When the largest stocks stumble, headline indexes tend to exaggerate the damage because those giants carry outsized weight.

Semiconductor shares were the market's biggest drag. The PHLX Semiconductor Index dropped 4.3%, with Nvidia, Broadcom, AMD, Intel, Micron, Sandisk and Seagate all losing ground. The slide showed how concentrated the risk had become in the chip trade, where a few mega-cap names can swing the entire sector's direction in a single session.

Hedge funds have also been quietly dialing back exposure. Goldman Sachs' prime brokerage said aggregate net positioning in its AI basket has fallen to its lowest level this year. That does not mean conviction is gone, but it does show that the crowded trade is becoming less crowded, which can either steady the market or leave it more vulnerable to a sharp reversal.

Even strong fundamentals could not stop the selling. TSMC posted its fifth straight quarter of record earnings, with profit surging 77%, yet the shares still moved with the broader chip rout. Meanwhile, South Korea tightened rules on leveraged chip ETFs after wild swings in SK Hynix and Samsung shares, a sign regulators are watching the leverage building in the trade.

Economic data offered little drama but added useful context. US retail sales rose 0.2% in June, cooling from May's revised 1% increase. Slower spending may ease inflation concerns, but it also reinforces the idea that economic momentum is gradually moderating. For equity traders, soft demand is a double-edged signal: good for rates, less good for the revenue outlook.

Futures pointed to another cautious start on Friday. Dow futures fell roughly 300 points, S&P 500 futures lost 0.7%, and Nasdaq futures dropped about 1% as traders digested another wave of corporate earnings. The pre-market reaction matters because it shows where risk appetite stands before the main US session, even if the cash open can diverge.

Netflix added to the cautious mood after shares fell more than 9% after-market despite reporting results broadly in line with expectations. The move is a reminder that in a nervous tape, even an in-line print can be punished if investors were hoping for more. With the biggest names reporting, the bar for a positive reaction has risen.

The earnings calendar is what makes this week different. The market is walking into a wall of results from the largest technology and financial names, and the tolerance for disappointment looks thinner after the recent tech wobble. Strong numbers could rebuild confidence, while weak guidance could accelerate the rotation out of crowded winners.

For index traders, the cleanest read is that the selloff is a repricing of crowded positioning rather than a sudden change in the macro story. The Nasdaq's 1.5% drop and the SOX index's 4.3% fall tell you where the pressure is concentrated. US500 traders can use the 0.7% S&P futures move as an opening risk gauge while watching whether megacap technology stabilises or extends lower.

Breadth is the detail worth watching. A small group of large companies can support headline levels while banks, industrials, and smaller technology names keep falling. If the selling stays narrow, dips may attract buyers; if it spreads, the index has further to correct. Cross-sector participation will decide whether Thursday's move was a shakeout or the start of something larger.

Risk control should account for event clustering. Earnings prints, retail data, and overseas headlines can all land outside US trading hours, and each can reprice the index fast. Rather than reading one overnight move as the full story, traders should wait for follow-through across sectors before drawing conclusions about direction.

Positioning into the move matters as much as the price. A market that enters a shock with crowded longs tends to fall faster, because leverage has to be unwound before any recovery can begin. A market that enters already de-risked can stabilise more quickly, because the weak hands have already exited. The recent tech concentration suggests the former risk is live.

The practical takeaway is to treat the week's action as a test of conviction rather than a verdict. A 1.5% Nasdaq decline is informative, but the cash session can diverge once earnings and the growth picture are in view. The most useful signals will be whether the index can hold a bid, whether chip stocks find support, and whether softer data keeps the rate story constructive.

MC Markets traders can use US500 to express a view on this cross-asset setup, tracking tech momentum, chip-sector volatility, and incoming earnings without taking on single-name risk. The Nasdaq's drop and the SOX slide put the concentration trade in focus, and this week's results will show whether the market's favorite winners can justify their weight. This is market commentary, not personal financial advice.

Trading Insight

The Nasdaq Composite fell 1.5% as a chip selloff intensified, with the PHLX Semiconductor Index down 4.3% and names from Nvidia to Micron all lower. The S&P 500 lost 0.5% and the Dow slipped 105 points, while Dow futures fell about 300 points and S&P 500 futures lost 0.7% into Friday. US retail sales rose 0.2% in June after May's revised 1% gain, and Netflix dropped more than 9% after-market. Watch chip breadth and earnings this week. This is market commentary, not personal financial advice.