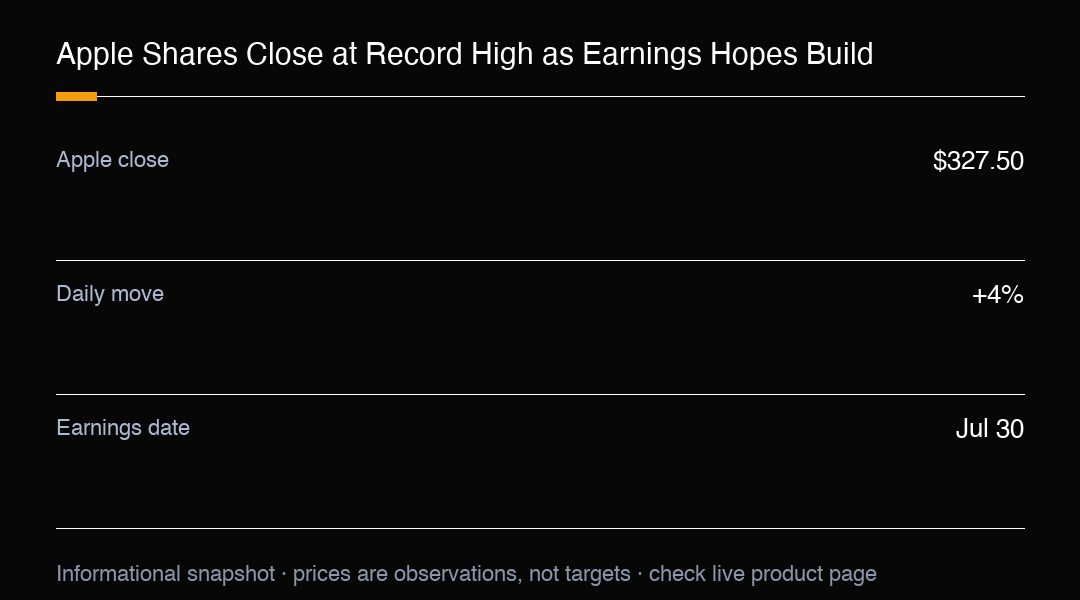

Apple shares climbed 4% to close at a fresh all-time high of $327.50, making it the strongest performer in the Dow and extending a sharp recovery just weeks after surprise price hikes had dented investor confidence.

The rally is notable because it comes from a company that was being questioned only weeks ago over broad price increases across its product lineup. Investors now appear willing to look past those concerns and focus on what comes next, with earnings due after the close on July 30.

Traders are betting Apple has the firepower to justify its premium valuation. A premium valuation simply means the stock already trades at a lofty price because the market expects strong future growth; that works well when the company delivers, and hurts when it does not, which is why the upcoming report carries so much weight.

One catalyst arrived from China, where regulators approved Apple Intelligence for rollout. The decision clears a major hurdle for the company's generative AI platform in the world's largest smartphone market, opening the door for AI-powered features, including an upgraded Siri experience, to reach millions of users who had been waiting for official clearance.

Smarter software gives Apple a fresh reason to convince users to upgrade their devices, which can lift hardware sales while strengthening its fast-growing services ecosystem. The AI green light arrived at a useful moment, just as attention turns to the quarterly report and the question of whether demand is accelerating.

Wall Street's focus is shifting to the earnings release. Investors want updates on iPhone demand, memory-cost pressures and whether consumers are still willing to spend despite sticky inflation. Each of those threads feeds directly into the margin story that analysts watch most closely.

Expectations are running high, and after a run to record territory, simply beating estimates may not be enough. The market has already priced in a strong quarter, so the reaction will hinge as much on what management says about the months ahead as on the numbers themselves.

Traders will watch forward guidance closely, since management's outlook for future sales and profits often moves the stock more than the headline results. Apple has won back the market's confidence, but record highs arrive with record expectations, and the earnings call will be the real test of whether the premium multiple is earned.

The China AI approval also reframes the competitive picture. With generative features now cleared for the largest smartphone market, Apple has a clearer path to monetise its software layer internationally, an angle that had been a known overhang for the shares.

For traders, the setup pairs a confirmed uptrend with a near-term binary event. A clean beat and confident guidance could extend the breakout toward the next leg higher, while any stumble against such elevated expectations may pressure the premium multiple quickly, making the July 30 print the decisive catalyst.

Options markets have priced in a sizable move around the print, reflecting how much is riding on the result. Implied volatility tends to compress after the call, but the direction of the post-earnings gap will be set by guidance more than by the quarter just reported.

Services revenue is the margin engine investors care about most. A rising services mix lifts overall profitability even if hardware units flatten, which is why the AI-enabled upgrade cycle is being watched as a potential accelerator rather than a one-off bump.

For traders new to the name, the takeaway is that a record high is not a reason to chase blindly. The catalyst is known and dated, so planning the reaction to guidance is more useful than guessing the entry ahead of the event.

The hardware cycle and the software story are converging at the right time. If the AI features land well in China, upgrade demand could lift both device sales and the higher-margin services tied to them, a combination the market rewards with richer multiples.

Cash returns remain a quiet backstop. Apple's scale of buybacks and dividends gives the shares a structural bid that many high-flying peers lack, which helps explain why dips have been bought so consistently during the recovery from the price-hike scare.

Bottom line for the trade: the trend is your friend into the print, but size the position for a guidance-driven move. The premium is earned or lost on the call, not on the run-up, so the plan should centre on the reaction, not the anticipation.

Watch the services margin commentary closely. Even a small beat on services profitability can justify a large part of the premium, because the market values recurring, high-margin revenue far above one-off hardware spikes, and that is where the AI story compounds.

In short, Apple's record is a vote of confidence that has been earned, not gifted. The earnings call is the moment that confidence is either reinforced with numbers or tested against the very expectations the rally has created, and the stock will trade the answer either way.

Ultimately, Apple's story is one of regained trust. The shares fell on pricing worries, recovered on earnings hope, and broke out on an AI clearance; the July 30 call is the checkpoint where that trust is either confirmed with numbers or questioned against the highest of bars.

Until the print, the path of least resistance is up, but the edge belongs to traders who plan the post-earnings reaction rather than the run-up. A recorded plan for both an upside and downside guidance surprise removes the temptation to chase at the worst moment.

The broader read is that quality at a premium is back in favour. After a year of punishing anything expensive, the market is again rewarding durable cash flows and ecosystem lock-in, and Apple sits at the centre of that renewed appetite for dependable growth.

Keep it simple: the trend is up, the catalyst is dated, and the plan should match. Trade the confirmation, not the guess, and let the July 30 guidance decide whether the record becomes a launchpad or a ceiling.

Trading Insight

Apple's breakout to a record high rides AI approval in China and earnings anticipation; the July 30 report and guidance are the next decisive catalysts.