IBM shares suffered their worst single session on record after a preliminary earnings warning tied to how enterprises are spending on artificial intelligence. The durable lesson for Nasdaq traders is not “AI is over” — it is comfort risk: narrative winners can re-rate violently when budgets re-prioritize inside the same AI boom.

For live index pricing on the growth sleeve most sensitive to that sentiment, see the NAS100 product page. Related reads: Nasdaq futures and oil risk-off and Nasdaq chip pullback and oil risk.

Key takeaways

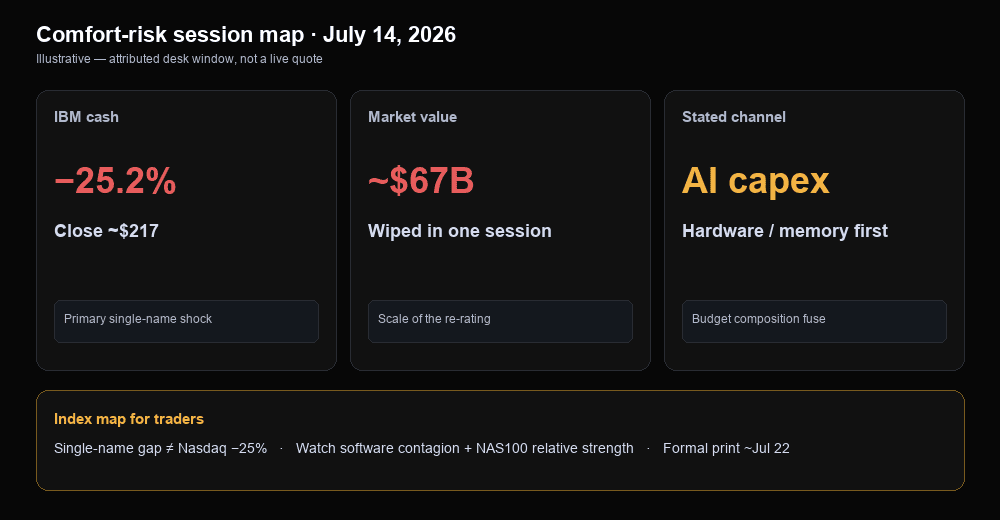

- IBM fell about 25% on July 14, 2026 after an AI-linked spending warning — a single-name re-rating, not a one-to-one Nasdaq crash template.

- The stated fuse was capex re-prioritization: clients shifted late-quarter spend toward AI hardware (servers, storage, memory) and delayed software/mainframe-linked deals.

- Near term: does software contagion hold, or does the move stay IBM-specific into the formal Q2 print?

Why did IBM stock crash 25%?

IBM crashed because management pre-announced a disappointing second quarter and explained a larger-than-expected shift in client spending toward AI infrastructure hardware — not because the cash market “randomly” deleted a quarter of the stock. According to Forbes coverage on Tuesday, July 14, 2026, IBM shares closed about 25.2% lower near $217, erasing roughly $67 billion of market capitalization and leaving the firm valued at just under about $205 billion. That session was worse than IBM’s Black Monday 1987 drop of about 23% and was framed across desks as the stock’s worst day in its modern history.

CEO Arvind Krishna’s investor letter — summarized the same day by Forbes and Reuters — said the quarter was “worse than our expectations,” that teams “faltered,” and that numerous large deals failed to close on expected timelines. The core transmission line: in the last weeks of June, clients shifted quarterly capex toward servers, storage, and memory to secure supply-constrained infrastructure ahead of expected price increases, pulling spend away from IBM’s software and infrastructure stack (including transaction-processing exposure tied to mainframe programs). Wall Street’s path into the formal report, via FactSet figures cited by Forbes, pointed to roughly $17.2 billion in quarterly revenue and $2.93 in earnings per share — with the full report expected around July 22, 2026.

What is “comfort risk” in the AI era?

Comfort risk is the gap between a popular AI-era narrative and the multiple the market will pay once cash-flow timing slips — even if the long-term AI story is still intact. Social market commentary framed the week with a blunt line: the biggest lesson of the AI era is never get comfortable. That is useful as a risk mindset, not as a price forecast. A name can look “AI exposed,” print strength earlier in the year, and still face a structural one-day re-rating when management admits it did not adapt fast enough to how clients are actually spending.

For traders, comfort shows up as three assumptions that fail together: (1) the AI label protects the valuation, (2) budget cycles are smooth, and (3) one strong narrative means low overnight gap risk. IBM’s session is a case study in how quickly those assumptions can reverse when a credible enterprise franchise says clients redirected spend inside the AI boom itself — toward hardware and memory, away from parts of the software stack.

How does AI spending pressure software stocks and Nasdaq exposure?

AI can pressure software stocks when enterprises divert near-term budgets to secure scarce infrastructure — even while total AI spending is rising. Reuters and WSJ-cycle coverage described the same channel: businesses racing for supply-constrained servers, chips, and networking gear divert spend from other technologies. That is a composition shock (where the budget goes), not automatically a proof that AI demand is collapsing.

Session reporting also noted a software-sector selloff and IBM as a major drag on the Dow Industrials, with other software names weak on the same tape (Fox Business and Guardian session notes). That contagion read matters for index traders: a single name can gap 25% without the Nasdaq 100 moving 25%, but software beta and growth-multiple sensitivity still show up in NAS100 relative performance when the market is pricing “who wins and who loses inside AI budgets.”

Keep the hierarchy clean. IBM is a single equity with its own mix of mainframe software, consulting, and infrastructure. The Nasdaq 100 is a diversified growth basket. Use IBM as a sentiment and budget-composition signal, not as a one-factor model for the whole index.

What should traders watch next?

Watch three confirmations: whether software contagion continues, whether NAS100 holds relative strength, and how IBM’s formal Q2 print updates the story.

Scenario A — contagion holds. Software peers stay soft, NAS100 underperforms broader US risk, and commentary keeps framing AI as a budget cannibal for non-hardware vendors. Dip-buying in growth can stay fragile until the market sees stable peer prints.

Scenario B — digestion. IBM remains the outlier, software peers stabilize, and NAS100 relative strength improves. That does not “prove” the AI cycle is healthy forever — only that the July 14 move is being priced as more idiosyncratic than systemic.

Scenario A fails quickly if software rebounds hard while IBM’s tape stabilizes and indices reclaim without software leadership on the downside. Scenario B fails quickly if peer software re-widens lower into IBM’s formal report and NAS100 leads a second leg of risk-off. Either path is conditional; neither is a trade instruction.

Session dashboard

| Market / item | Read (window) | Role |

|---|---|---|

| IBM cash equity | ~−25.2% to ~$217 (Jul 14, 2026 close) | Primary single-name shock |

| IBM market value | ~$67B wiped; firm ~<$205B (same window) | Scale of the re-rating |

| Stated channel | Late-June capex shift to servers / storage / memory; delayed deals | AI budget composition fuse |

| Formal print path | ~$17.2B rev / ~$2.93 EPS (FactSet path); report ~Jul 22 | Next hard update |

| Software tape | Sector sold with IBM; IBM a major Dow drag (session notes) | Contagion check |

| NAS100 map | Index beta to growth/software sentiment — not 1:1 with IBM | Index expression for traders |

Session prices move over the day and across sessions — later levels may differ. Live index quotes: NAS100.

Final thoughts

IBM’s session is a reminder that the AI boom still has winners and losers inside the same budget cycle. A name can sit inside a popular narrative and still re-rate hard when management admits client spend moved faster than the franchise did. For Nasdaq-facing traders, treat that as a comfort-risk lesson: watch how software peers and NAS100 relative strength behave into the formal print, and keep single-name gaps from becoming an automatic index forecast.